Blog Item

Why banks must become the data custodian in the data economy

The rising importance of digital identity, consent management and data sharing has created a ‘Blue Ocean’ market for banks. I believe that they now have a unique opportunity to strengthen and truly safeguard their relevance in the data economy. But they need to start taking decisive action right now in order to demonstrate that they can provide the necessary trust.

The European Payments Initiative (EPI) is an important collaboration platform and a clear step in the right direction. However, the banks involved in the EPI currently appear to be focused on protecting the payments business case in Europe. While this is understandable, such defensive tactics in the ‘Red Ocean’ payments market is not really a viable long-term strategy. The good news is that, as we see it, the EPI also paves the way for strengthening the banks’ future relevance – beyond payments alone.

The opportunity for banks to secure their future relevance

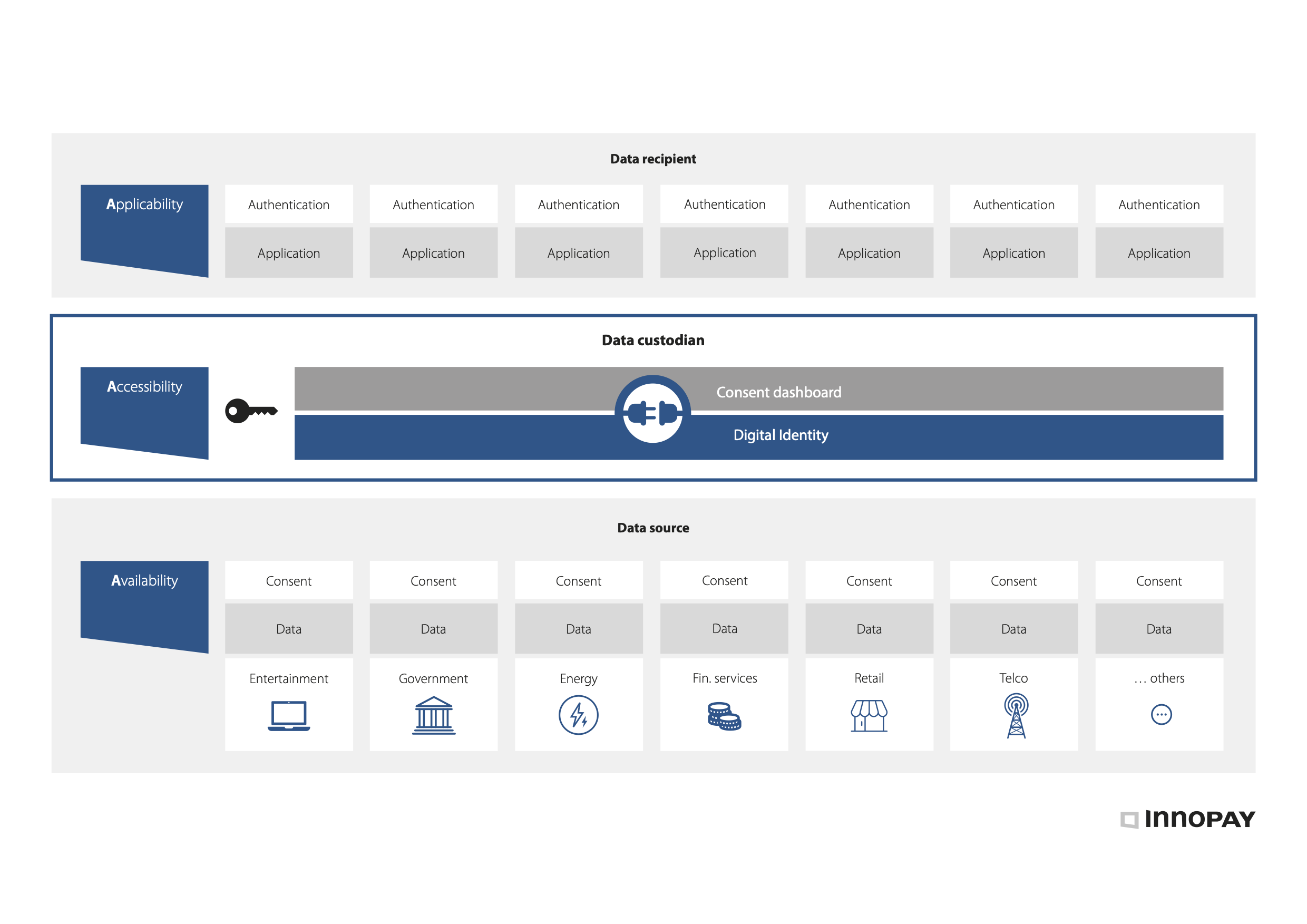

Regulatory reforms such as PSD2, Open Banking, GDPR and developments such as the EU Data Strategy are democratising access to data assets across the whole economy. In this changing world, banks now facilitate only a fraction of a customer’s (daily) digital interactions and transactions. However, as money custodian, banks are ideally placed to expand their role into the data domain. In other words, we believe that banks can – and should – lay claim to the role of ‘data custodian’ in their customers’ daily lives by engaging in a cross-sectoral data ecosystem (see Figure 1) – just as they do in their current role in payments.

Ultimately, the role of data custodian will help to secure the future relevance of banks in the data economy in several ways, including by:

- Offering better protection of user data and privacy

- Driving innovation in digital transaction services (payments and beyond)

- Stimulating the creation of new business models and monetisation options

- Effectively shielding them against threats coming from Chinese and US big-tech firms.

Figure 1: Banks acting as data custodian in the data economy

The shifting data-benefit balance

In a changing world in which data is emerging as the new global currency and digital transactions are at the heart of everything we do, customers are becoming more aware of their data assets and the value it represents; they want to leverage their data beyond the platforms and organisations that store it in order to tip the ‘data-benefit balance’ back in their favour. This is driving customer demand for increased transparency and control over their data assets – which is also known as ‘data sovereignty’.

As a result, we are seeing an emerging need for a data custodian like role to ensure seamless and secure access in a trusted and well-governed ecosystem which revolves around digital identity and consent. Trust provision will be a key functional domain. The data custodian will meet the growing desire among customers to have a single point of control for their data assets, including by giving customers the required tools to exercise control over them. In addition, as customers become accustomed to controlling and sharing their data on their own terms, the increased trust will open up new opportunities to engage in ways that create customer-centric data monetisation models and a fair distribution of the benefits.

The three key beliefs shaping the future relevance of banks

Against the backdrop of the current transformation, we believe that the future relevance of banks will be shaped by the following three beliefs:

- Although important, digital payments – and related collaborations (e.g. EPI) – are not sufficient for banks to remain relevant in a world in which everything is a digital transaction

- Banks are ideally placed to unlock the potential of the open data economy by creating a digital trust infrastructure and become society’s everyday data custodian

- In an open data economy, a bank’s digital identity and consent management services are key in facilitating trusted financial and non-financial digital transactions in all areas of society.

So bank executives face a choice. They can either ignore the digital transaction revolution and stick to their existing beliefs, continuing to invest in payments only and competing head-on with big-tech and other players in a Red Ocean market… or they can embrace the above beliefs to seize the Blue Ocean opportunity, expanding their role as money custodian into the data domain to secure their future relevance in the data economy.

Becoming a data custodian in the data economy is a longer-term play; it requires bank executives to embark on strategic initiatives that do not necessarily contribute directly to short-term regulatory compliance and/or ROI. However, doing nothing is not an option as the true battle for relevance revolves around digital identity, consent and data sharing – where even more value is at stake than in payments. As big-tech firms and other providers are already making inroads into these areas, there is no time to waste.

Leaders at any bank wishing to participate successfully in this new environment will need to review their strategies as well as their technological and operational capabilities. Banks will have to recognise that putting customers in control of their money and data is imperative for future strategic and commercial relevance.

Related publications

Publication

|

Blog

COMPANIES CAN MAKE PURSUING SUSTAINABILITY MORE SUSTAINABLEMany companies made promises to shareholders and the public to pursue sustainability. While most are trying to fulfill their pledges despite some relaxation in mandates, they aren’t finding it easy. The market has tried to help by developing decarbonization claims that allow busin...

read more

Publication

|

Blog

The topic of artificial intelligence dominates boardroom discussions, yet most organizations are struggling to unlock its full potential. Research by RAND shows that up to 84% of AI projects fail to scale to deliver enterprise-wide impact (RAND, 2024). A recent study from MIT reveals even higher figures, finding that 95% of...

read more

Publication

|

Interview

The European financial sector is entering a new era of data-driven innovation. T...

read more

Publication

|

Blog

In the wake of the digital revolution, the money landscape is rapidly evolving. ...

read more

Publication

|

Blog

Given recent developments around the introduction of Section 1033 in the US, this blog takes a closer look at the current state of Open Banking in the country.To do so, we will apply INNOPAY’s Open Banking Monitor (OBM). Since 2017, the OBM has provided global insights into the industry by analyzing various developer experience features -...

read more

Publication

|

News

A new report commissioned by the Euro Banking Association outlines the strategic...

read more