Blog Item

Mastering the evolved blockchain space – 2025 update to INNOPAY’s Digital Assets Ecosystem Scan

INNOPAY launched its Digital Assets Ecosystem Scan in 2023. Designed to visualise the complex landscape of digital assets in a single, indicative overview, it serves as a compass for navigating this emerging space. In our earlier article reviewing last year’s major events, we observed a rapid evolution of the sector. This underscored the need for us to update our original ecosystem overview.

In this article, we guide you through the significant industry changes we have observed since 2023, using the updated Digital Assets Ecosystem Scan*. We identify three key trends:

- Exponential growth and maturation across all layers of the ecosystem

- Increasing institutional adoption, and

- Initial emergence of synergies between digital assets and artificial intelligence (AI).

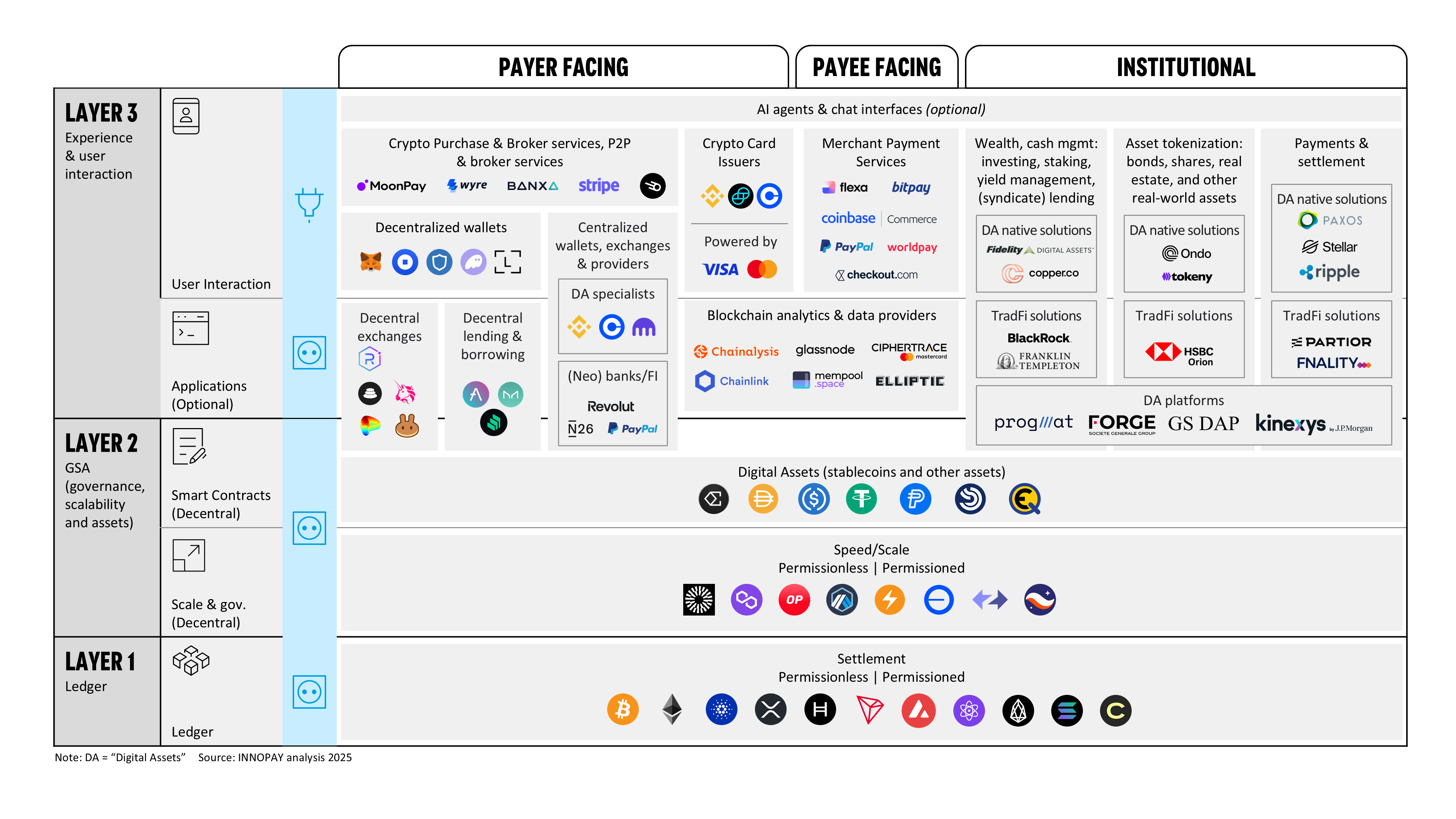

Recap: What is the Digital Assets Ecosystem Scan?

The Digital Assets Ecosystem Scan depicts the layered structure of today’s digital assets landscape. Like the internet’s TCP/IP model, the digital assets ecosystem consists of interconnected layers, each serving specific functions.

These are the three main layers:

Layer 1 is the ‘ledger’ layer that processes and finalises transactions, ensuring security and integrity. Since each blockchain ledger has unique characteristics, Layer 1 targets various use cases. This usually means a trade-off between decentralisation, security and scalability.

Layer 2 solutions – such as the Lightning Network for Bitcoin or Arbitrum for Ethereum – are built on Layer 1 to enable faster transactions and reduce costs. This layer also includes smart contracts, which automate processes and enable trustless interaction with decentralised services.

Layer 3 is where users interact with digital assets. It includes user interface (UI) and user experience (UX) components. Layer 3 plays a crucial role in driving adoption by simplifying user interactions. Decentralised finance (DeFi) applications flourish in this layer, offering user-friendly platforms for services such as asset custody, trading and lending. While users can engage directly with the blockchain, this approach can be cumbersome, highlighting the need for effective services within Layer 3. This layer is also where traditional finance (TradFi) can offer compelling user propositions, obfuscating the complexity and usability risks of DeFi.

*Please note that the scan serves as an attempt to capture the complex digital assets space in a single, indicative overview and should by no means be interpreted as an exact, exhaustive representation.

Key ecosystem changes since 2023

These are the three key changes compared to the 2023 ecosystem scan:

- Exponential growth and maturation across all layers

- Increasing institutional adoption

Initial emergence of synergies between digital assets and AI

1. Exponential growth and maturation across all layers

An overall trend we observe is the increased activity across all layers – both in terms of usage volumes and number of offerings – and the maturation of solutions.

In terms of blockchain networks, we witness a rise of DeFi applications built within the ecosystem built on the Ethereum Layer 1 ledger. Ethereum is attractive due to its smart contract functionality, network size and security, combined with the lower costs and enhanced speed of Layer 2 solutions. From more of a ‘retail’ perspective, the ecosystem built on the Solana Layer 1 ledger is experiencing heightened activity.

The usage of decentralised services in Layer 3 such as the exchanges Raydium and Jupiter, along with wallets like Phantom, is growing significantly. This surge is largely driven by interest in ‘meme coins’, which reached a peak with the launch of US President Trump’s TRUMP coin. Solana’s increasing popularity can be attributed to its user-friendly interface, performance and accessibility, allowing users to participate within minutes by simply downloading an app and accessing services at very low fees. However, it remains uncertain whether a broader audience – especially institutional players, who are more sensitive to governance and compliance – will fully embrace Solana, as Ethereum continues to dominate the market with a total value locked (TVL) nearly ten times greater than that of Solana.

Furthermore, stablecoins – which can be issued on both Layer 1 and Layer 2 networks, depending on design choices and use case – are experiencing a remarkable surge with their market cap skyrocketing to USD 250 billion. While the market remains dominated by blockchain-native USD powerhouses Tether and Circle, new institutional entrants such as PayPal and Société Générale are rapidly emerging, often targeting different, institutional use cases.

2. Increasing institutional adoption

Institutional stablecoin issuers exemplify a broader trend of TradFi players embracing digital assets solutions, as illustrated by the addition of a new quadrant in the top right corner of our scan. Inherent benefits of blockchain technology – such as speed, 24/7 availability, low cost, interoperability, global access and automation – enable disruptive alternatives to traditional financial services. Initial reluctance to engage with digital assets has diminished due to technological maturity, rising client demand, political momentum, and regulatory clarity and legitimisation, e.g. through the introduction of crypto exchange-traded funds (ETFs) in the US and the Markets in Crypto-Assets Regulation in Europe.

In the Digital Assets Ecosystem Scan, we have categorised activity in three key areas:

Wealth and Cash Management – optimising the management of financial assets through blockchain technology, encompassing investing, staking, yield management and treasury services.

Asset Tokenisation – the digitisation of bonds, shares, trade documentation, real estate and other so-called real-world assets, providing benefits like easier transferability, improved transparency and atomic settlement through an on-chain cash leg (see ‘Payments and Settlement’).

Payments and Settlement – executing financial transactions on a blockchain, often utilising stablecoins, which removes traditional frictions – particularly in cross-border transactions – through 24/7, cheaper, faster and programmable payments to recipients anywhere in the world.

Within these three areas, we observe specific solutions offered by both blockchain-native and TradFi players. Meanwhile, large institutions like J.P. Morgan and Société Générale offer a comprehensive suite of services across all three areas through a single ‘digital assets platform’. This enables them to serve a broad range of clients such as corporates, other financial institutions and public entities like central banks.

3. Initial emergence of synergies between digital assets and AI

AI is making waves across all markets, and the world of digital assets is no exception. AI is a great fit with the blockchain ecosystem, which is entirely digital and offers opportunities for automation. Although this development is still in the early stages, we are beginning to see promising solutions emerge, such as analytical tools and task automation services like Trojan, which assists in trade execution. Furthermore, AI agents serve as the perfect assistants to interact with digital assets. These are represented by an additional UI layer in our scan. While many applications are still experimental and primarily used by retail innovators, they possess the potential for rapid evolution, which we expect to unfold at an accelerating pace. We envision a future scenario where users can simply ‘talk’ or ‘chat’ with their AI assistant to manage on-chain tasks, such as gaining market insights, making payments or overseeing their organisation’s operations.

Closing thoughts

As outlined in this article, the digital assets landscape has undergone significant evolution in the past two years, characterised by three key trends: growth and maturation across all layers, institutional adoption, and the emergence of AI within digital assets. At INNOPAY, in collaboration with our partners, we remain committed to closely monitoring this ongoing (r)evolution of financial services and its implications for the financial sector at large.

This article was originally published at The Paypers.

Related publications

Publication

|

Blog

Most companies want to decarbonize their product lines and operations, whether because of smart risk management, shareholder pressure, or regulatory mandates. But decarbonizing is often expensive, with slower returns on investment, in part because of regulatory volatility. This has prompted many enterprises to struggle to find the “r...

read more

Publication

|

News

Access to financing remains one of the biggest hurdles for European small and me...

read more

Publication

|

Blog

COMPANIES CAN MAKE PURSUING SUSTAINABILITY MORE SUSTAINABLEMany companies made promises to shareholders and the public to pursue sustainability. While most are trying to fulfill their pledges despite some relaxation in mandates, they aren’t finding it easy. The market has tried to help by developing decarbonization claims that allow busin...

read more

Publication

|

Blog

The topic of artificial intelligence dominates boardroom discussions, yet most organizations are struggling to unlock its full potential. Research by RAND shows that up to 84% of AI projects fail to scale to deliver enterprise-wide impact (RAND, 2024). A recent study from MIT reveals even higher figures, finding that 95% of...

read more

Publication

|

Interview

The European financial sector is entering a new era of data-driven innovation. T...

read more

Publication

|

Blog

In the wake of the digital revolution, the money landscape is rapidly evolving. ...

read more