Blog Item

Three Go-To-Market approaches for banks to play in the Embedded Finance space

Embedding financial services at the point of need is one of the most exciting developments within the digital finance space right now. With new use cases and partnerships being announced almost daily and projected revenues generated through Embedded Finance (EmFi) north of a €100 billion in Europe, many banks feel the urge to explore if and how they can benefit from this development and stay relevant for customers.

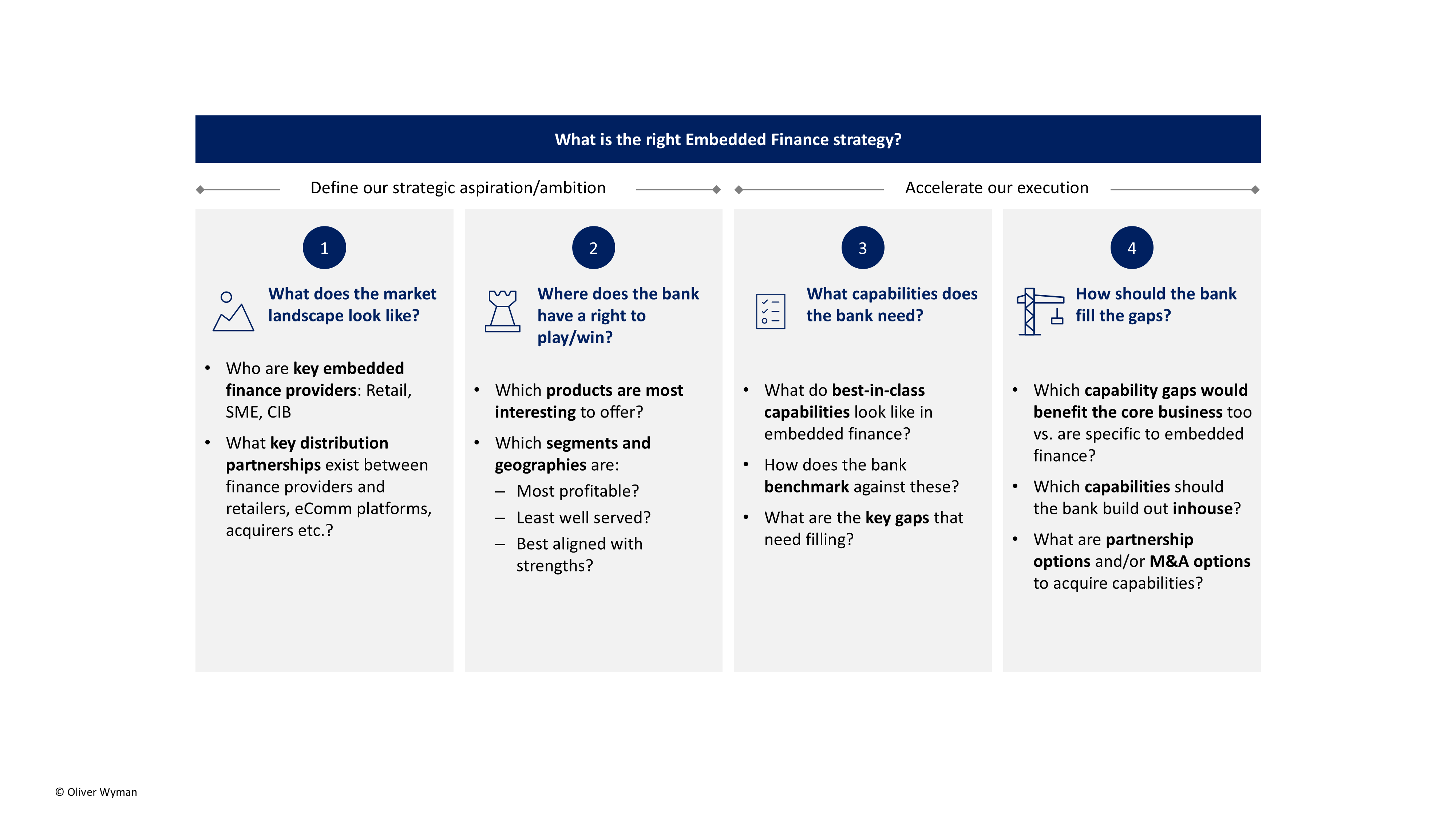

In 2024, we’ve worked together with our clients to find answers to essential questions to define a fit for purpose Embedded Finance strategy for their business. The figure below illustrates a typical approach.

Figure 1: Building blocks to design the right Embedded Finance strategy

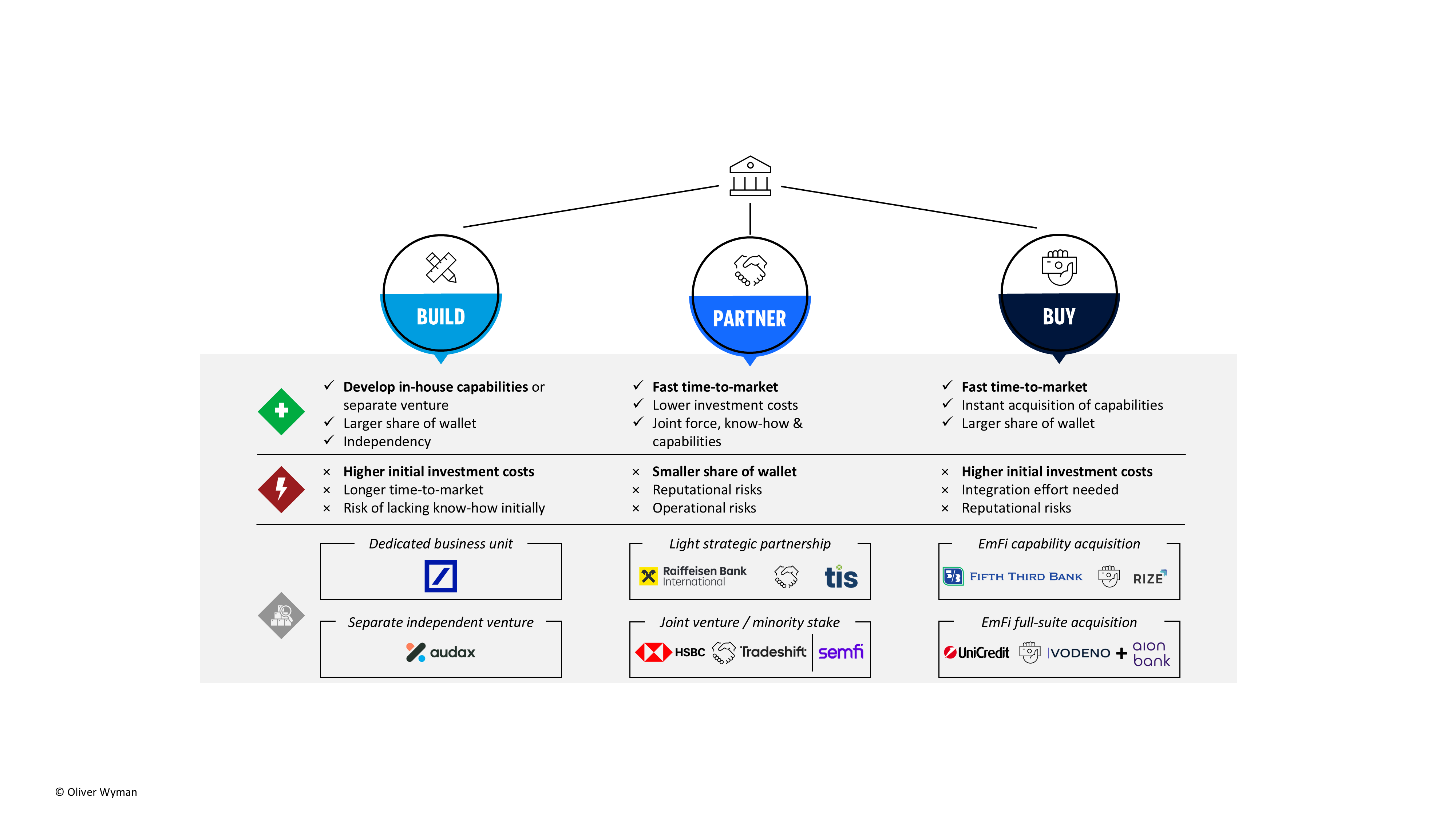

This blog reflects on some of the options and observations regarding the fourth step of the approach. Our Embedded Finance radar – in which we keep track of emerging business models and partnerships – has revealed insights that incumbent banks broadly take 3 different approaches to play in the EmFi space. The options are shown in the visual below.

Figure 2: GtM approaches for banks to play in Embedded Finance

A. Build

Setting up a dedicated business unit or launching a new venture within a group can help to bundle resources to build capabilities and know-how in-house. This mitigates the risk of dependencies with other partners or acquired businesses. Furthermore, full share of wallet remains at the bank. Typically, banks either keep the business unit in-house or separate it into an independent venture, that is not burdened by corporate processes. This approach can also change along the way, as described in the case study further below in this blog.

However, this is typically associated with higher investment costs and longer time-to-market, as capabilities need to be developed in-house and require therefore patience, senior executive commitment and willingness to invest.

Case study - Build

Standard Chartered (SC) started its embedded finance journey in Asia through its innovation arm SCVentures in 2020, with the launch of SC Nexus, a white-label BaaS-platform that enabled clients to integrate SC’s financial services. After initial successful partnerships with large e-commerce platforms in Asia, SC decided to further leverage the tech-capabilities and bundle these in a separate venture – audax. Audax can now grow with less corporate hassle and can support both SC’s clients directly or function as accelerator for other financial institutions that want to drive their own digital transformation or BaaS-related business models.

B. Partner

A less investment-heavy approach is to join forces with other relevant tech providers – thus combining capabilities and know-how of both parties.

Next to a shorter time-to-market, financial services can also be tailored and further enhanced through partnering, as additional data or features can complement the core financial product. In practice, two different approaches can be observed – forming a “lighter” partnership, mainly consisting of e.g. a referral model and maybe some joint marketing towards clients versus moving into more advanced partnership models, i.e. joint ventures, where a bank takes a (minority) stake in a tech company (BaaS provider), which is further described in the case study below.

Partnerships however come with dependency risks that need to be mitigated – both from a reputational, operational point of view (e.g. unforeseen technical issues or lack of compliance) and strategic perspective (e.g. exclusivity of partnership and consequences and exit strategies when the partner is acquired by a direct competitor). Furthermore, agreements need to be made regarding the distribution of revenue between involved parties.

Case study - Partner

In October of 2024, international bank HSBC and supply chain financing platform Tradeshift announced their joint venture SemFi, which will provide embedded financial products for businesses using B2B e-commerce marketplaces, including that of Tradeshift. This joint venture will enable sellers to receive early invoice payments with competitive credit limits from HSBC or other banks, all powered by their ability to leverage transaction histories and account data. While SemFi is initially only available in the UK, they are looking to ultimately expand into the full range of HSBC’s operational regions.

C. Buy

The final method, which involves purchasing an existing provider, combines elements of the first two strategies, as capabilities and know-how are being acquired almost instantly, bundled in a dedicated team with experience and clear strategy on the market offering. This can either be an acquisition of a niche capability provider, focused on a specific service like payments or specific industry like energy, or the acquisition of multiple providers to enable a full-suite EmFi offering (see case study below).

Same as with the build-option, these efforts usually go hand in hand with higher investment cost needed upfront. Post merger integration and operating model considerations need to be carefully assessed to maintain the agility, flexibility and rapid go-to-market approaches of the acquired asset(s).

Case study - Buy

By acquiring Vodeno & Aion Bank in the summer of 2024, UniCredit instantly expanded their capabilities by combining digital banking services from Aion Bank based on a fully fletched, API-based BaaS-platform from Vodeno. Through the acquisition, UniCredit can provide a broad palette of financial services, ranging from accounts to payments, embedded within any distributing platform, from retailers to other financial service providers.

Conclusion

Banks are in the driving seat to determine their embedded finance strategy. However, as the pace of new market entrants continues, banks risk losing a significant part of their current revenue streams as embedded models are gaining traction across financial products. Therefore, banks should carefully consider their embedded finance strategy starting with developing a solid understanding of the market, where to play and how to win.

INNOPAY’s Embedded Finance Radar tracks EmFi trends and developments

The radar tracks evolving use cases, and the players involved throughout the value chain and around the globe, across six product categories (e.g. payments, lending) and six major industries (e.g. retail & ecommerce). For more details or insights, please reach out to Mounaim Cortet, Patrick de Haan, or William Hanley.

Related publications

Publication

|

Blog

COMPANIES CAN MAKE PURSUING SUSTAINABILITY MORE SUSTAINABLEMany companies made promises to shareholders and the public to pursue sustainability. While most are trying to fulfill their pledges despite some relaxation in mandates, they aren’t finding it easy. The market has tried to help by developing decarbonization claims that allow busin...

read more

Publication

|

Blog

The topic of artificial intelligence dominates boardroom discussions, yet most organizations are struggling to unlock its full potential. Research by RAND shows that up to 84% of AI projects fail to scale to deliver enterprise-wide impact (RAND, 2024). A recent study from MIT reveals even higher figures, finding that 95% of...

read more

Publication

|

Interview

The European financial sector is entering a new era of data-driven innovation. T...

read more

Publication

|

Blog

In the wake of the digital revolution, the money landscape is rapidly evolving. ...

read more

Publication

|

Blog

Given recent developments around the introduction of Section 1033 in the US, this blog takes a closer look at the current state of Open Banking in the country.To do so, we will apply INNOPAY’s Open Banking Monitor (OBM). Since 2017, the OBM has provided global insights into the industry by analyzing various developer experience features -...

read more

Publication

|

News

A new report commissioned by the Euro Banking Association outlines the strategic...

read more