Blog Item

How e-invoicing mandates in Europe are opening the doors to embedded lending

The introduction of e-invoicing mandates in the EU is driving substantial changes in the B2B ecosystem, particularly for SMEs. As e-invoicing becomes the standard, SMEs will increasingly adopt software to manage various business processes, including contracting, invoicing and payment. This is enhancing the availability and accessibility of valuable, authentic and certified data on B2B transactions, unlocking opportunities for embedded lending. Traditional players and fintechs alike need to adapt by providing innovative financing solutions and forming partnerships that capitalise on the data generated by e-invoicing.

E-invoicing: a game changer for SMEs

Many European Union (EU) countries are introducing mandates for business-to-business (B2B) e-invoicing, following the lead of Italy which did so in 2019. For example, mandates will come into force in both France and Belgium in 2026. As a result, small and medium-sized enterprises (SMEs) will be required to use software solutions for e-invoicing. This creates significant potential for e-invoicing providers such as vendors of accounting software, order-to-cash/procure-to-pay software and enterprise resource planning (ERP) software.

Data availability and accessibility fuels embedded lending

Delivery, invoicing and payment are decoupled in time in B2B trade interactions, with payment typically due after 30 days. This can create cashflow problems for sellers, for example in sectors with seasonal demand. Therefore, effectively managing working capital is one of the most pressing concerns for SMEs.

Financing solutions such as factoring and supply chain finance can help SMEs to manage their working capital needs to some extent. These traditional financing solutions – which are more relevant for the sell side of the business – also present significant disadvantages for SMEs. For instance, access to factoring and supply chain finance is often limited due to complex creditworthiness assessments and high fees. Additionally, these solutions require substantial administrative effort and can lead to a loss of control over the SME’s relationships with buyers and suppliers.

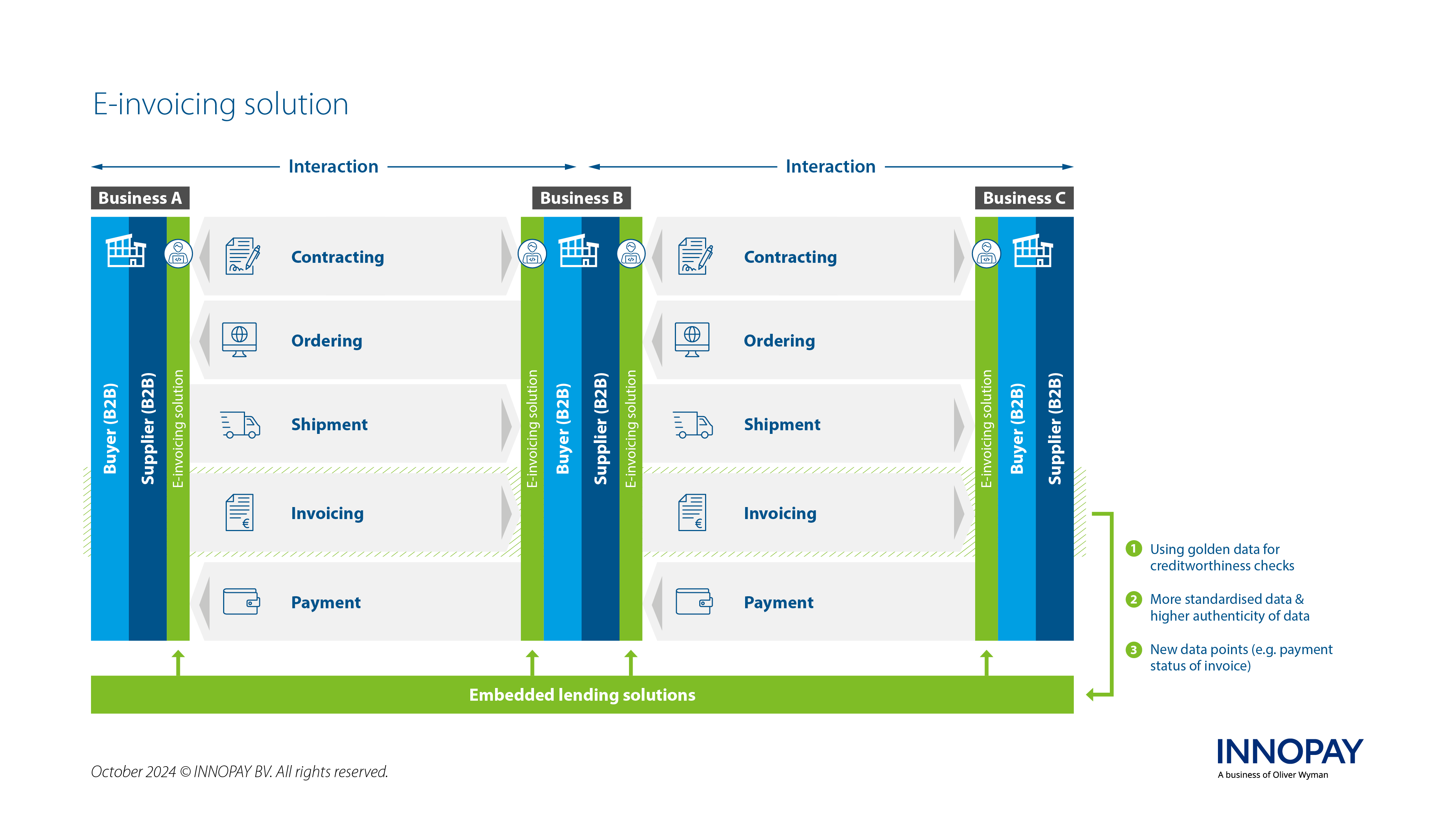

The increased availability of standardised data resulting from e-invoicing offers a promising opportunity to address these disadvantages with embedded lending (see figure). After all, e-invoicing improves the authenticity of invoice data – particularly in countries like France, where government-certified e-invoicing providers (PDPs) must be used. Additionally, new relevant data will become available, including invoice status (accepted/rejected), payment status (approved, paid), transaction history and customer preferences.

Individual invoices can become high-quality collateral when there is minimal uncertainty about their existence and payment status. To facilitate embedded lending, this ‘golden data’ obtained from e-invoicing providers can be leveraged for risk assessments, for example.

Figure: How data from e-invoicing can be leveraged for embedded lending solutions.

Traditional players need to redefine their position and offering

Ultimately, SMEs will seek the most convenient ‘one-stop-shop’ solution for e-invoicing – one that encompasses all services related to B2B interactions, including contracting, ordering, shipping, invoicing and payment (see figure). As the opportunities for embedded lending grow, e-invoicing providers are well placed to expand their financing options beyond traditional solutions, and offer SMEs improved solutions for managing working capital for both the sell side and the buy side of their business. Meanwhile, traditional financing providers such as banks and factoring companies will thus be facing increased competition. This could disrupt their existing relationships with SMEs.

To remain competitive, traditional players should consider the following actions:

1.Explore strategic partnerships

Identify potential collaborations with e-invoicing providers to enhance their relevance, value add and reach to SME clients. E-invoicing providers benefit from this strategic partnership as it provides opportunities to become the one-stop-shop solution for their customers, by seamlessly integrating lending propositions into their software solutions.

2.Improve financing products

Innovate existing creditworthiness assessments and minimise the administrative burden for SMEs to onboard for financing products.

3. Expand their role in the ecosystem

Consider diversifying their role in the e-invoicing ecosystem to strengthen their position in SME financing. For example they could move beyond strategic partnerships and establish themselves as an e-invoicing provider. There are numerous examples of banks that are integrating e-invoicing solutions through M&A or strategic investments (e.g. Credit Agricole & Kolecto or BPIFrance & iPaidThat).

Are you curious about how e-invoicing can unlock new opportunities in embedded finance and payments? Reach out to Mounaim Cortet and Jorrit Penninga to learn more.

verwandte Publikationen

Publication

|

Interview

The European financial sector is entering a new era of data-driven innovation. T...

Lesen Sie mehr

Publication

|

Blog

COMPANIES CAN MAKE PURSUING SUSTAINABILITY MORE SUSTAINABLEMany companies made promises to shareholders and the public to pursue sustainability. While most are trying to fulfill their pledges despite some relaxation in mandates, they aren’t finding it easy. The market has tried to help by developing decarbonization claims that allow busin...

Lesen Sie mehr

Publication

|

Blog

The topic of artificial intelligence dominates boardroom discussions, yet most organizations are struggling to unlock its full potential. Research by RAND shows that up to 84% of AI projects fail to scale to deliver enterprise-wide impact (RAND, 2024). A recent study from MIT reveals even higher figures, finding that 95% of...

Lesen Sie mehr

Publication

|

Blog

In the wake of the digital revolution, the money landscape is rapidly evolving. ...

Lesen Sie mehr

Publication

|

News

A new report commissioned by the Euro Banking Association outlines the strategic...

Lesen Sie mehr

Publication

|

Blog

Stablecoins are entering mainstream finance, offering the potential to make the ...

Lesen Sie mehr