Blog Item

Decentralised Finance is facilitating successful innovation by enabling ‘more for less’

Blockchain, Bitcoin and Decentralised Finance (DeFi) are all relatively new terms in today’s commercial vocabulary. Although their impact on the future of business is not yet entirely clear, at INNOPAY we believe that the genie is out of the bottle. The shift from institutional (centralised) to infrastructural (decentralised) trust is now unstoppable, and it marks a turning point in the history of finance. Decentralised technologies are set to revolutionise the global financial system and its institutions. This article explains more about how infrastructural trust works and explores the opportunities of DeFi for the financial sector.

In a recent article, the Harvard Business Review predicted that the current economic situation caused by the COVID-19 pandemic will “hasten the progress to more decentralised value chains”. Indeed, the current focus on decentralised technologies such as blockchain and Bitcoin is part of a general global tendency towards decentralisation of technology, functionality and business models which can be seen in several domains, including energy, social media, music and broadcasting. Meanwhile, in the finance sector, cryptocurrencies such as Bitcoin and the underlying blockchain protocols are driving the shift to Decentralised Finance.

Bitcoin: the first introduction to infrastructural trust

Decentralised Finance (DeFi) is a permissionless infrastructure, fully secured by encryption, that enables people and businesses to perform transactions directly with each other, without needing institutions to act as intermediaries. The roots of DeFi can be found in the 2008 Bitcoin whitepaper that set out a new system for digital cash. Bitcoin made it possible to transfer value between two ‘peers’, through open-source software and without a sign-up process (i.e. permissionless), by building trust into the technology and the governance behind it. This was the world’s first introduction to cryptocurrency and the concept of infrastructural trust.

This infrastructural trust is based on a number of concepts:

1. Digital scarcity

The concepts of digital ‘scarcity’, digital ‘uniqueness’ and digital ‘ledger’ are foundational for Bitcoin and many other blockchain-based cryptocurrencies such as Ethereum, Binance Coin, Solana and Stellar. In the past, nothing digital could be ‘scarce’ because digital things could easily be copied or altered. As a result, it was impossible to trust anything digital, since it could be a fake.

Digital scarcity was pioneered by Bitcoin. It proved that digital assets can be owned and transferred simply by controlling the cryptographic keys of an address. In the case of Bitcoin, a network of verifiers (‘miners’) produce an update of the decentralised ledger approximately every 10 minutes, in order to secure the ledger.

Together with the smartly designed incentive structure (by the competitive and energy committing consensus), Bitcoin has clearly proved its scarcity, as underlined by recent spectacular increases in its price (up to US$60,000 as of October 2021). This scarcity allows digital representations of value, data and physical objects to be controlled by end-users through the possession of digital keys. Other cryptocurrencies and blockchains have emerged since Bitcoin, all with different design choices, levels of adoption and success. Ethereum is currently the second largest after Bitcoin, followed by Binance and Solana.

Intermediaries such as specialised and regulated service providers (e.g. Coinbase, Kraken, Binance and Gemini, to name but a few) can be used at the end-user’s discretion in order to make it easier to manage and operate blockchain accounts. This can be beneficial since the security features make them cumbersome to use and error-prone, which in turn can lead to loss of funds. In a way, this is similar to how money is dealt with today; users can hold cash themselves, but also have the option to enlist a bank’s help to hold and manage cash for them.

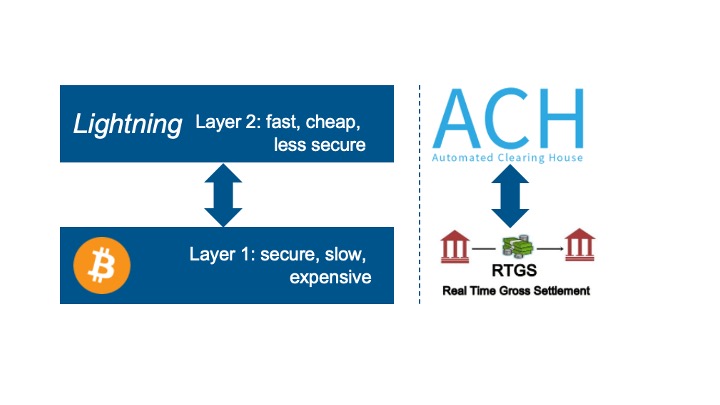

2. Layer 1 and 2 protocols

In a decentralised ecosystem, there are two types of protocols. A Layer 1 protocol refers to a blockchain, and a Layer 2 protocol refers to a third-party integration that can be used in conjunction with a Layer 1 blockchain.

It is important to understand this distinction. Layer 1 protocols are the base security layers of cryptocurrencies such as Bitcoin, Ethereum and the newer offerings by Binance and Solana.

However, as the number of users grows, the transactional capacity of the underlying blockchain fills up. This leads to higher transaction fees and lower throughput. The goal of the Layer 2 protocol is to improve the transaction speed at lower fees, thus allowing scalability, at the expense of a reduction in centralisation and security.

Figure 1 – Layer 1 and 2 protocols in DeFi and its analogy in the current financial system.

The Layer 2 protocol for Bitcoin is called the Lightning protocol. Ethereum has various scaling options and combinations, including Plasma, Flexa and xDAI. In the case of payments, these protocols are for users to transact, by netting transactions across various ‘nodes’. Nodes receive a small fee for backing full or partial transactions with Layer 1 assets (e.g. Bitcoin and Ethereum). Layer 2 solutions are live, but are in continuous development while in use (as is almost everything in the blockchain realm). As Bitcoin usage continues to grow over time, more value is being entrusted to the Lightning network (approx. US$200 million in October 2021 in order to secure faster value exchange. The Ethereum Layer 2 ecosystem is approximately a thousand times bigger (US$200 billion in October), mainly because these Layer 2 protocols primarily relate to services other than payments.

The natural trade-off of these two protocol layers is security, adding to the infrastructural trust. This can be likened to Real Time Gross Settlement (RTGS) systems and the Automated Clearing House (ACH) set-up in the traditional payments world. ACHs aggregate payment balances between banking participants (netting) and input the resulting value transfer to the RTGS system for final settlement (see Figure 1).

3. Governance of blockchains

Governance of a blockchain is a key determinant for infrastructural trust – for its security, robustness and level of decentralisation. A community decides on technical, procedural and legal matters in order to create, maintain and advance the blockchain. The governance process is essential. Agreement must be reached on topics such as: Who can decide on what? Who appoints whom? And who can initiate discussions? In many blockchains, this process is rather opaque since in practice a small group of people may influence the course of the blockchain. Due to its extreme decentralisation, Bitcoin seems to have the greatest lack of governance, making it very slow to change. Some regard this as a bug, others as a feature.

In order to improve on transparency of governance, several projects (such as Aave, Compound, Uniswap and Sovryn) have introduced ‘governance tokens’ as a way for community members to participate. Governance tokens allow holders to have control by being able to vote on changes to the protocol and thus to contribute to decisions about the future of the protocol and improving the infrastructural trust.

4. Smart contracts

Smart contracts have been pioneered by Ethereum, which was launched in 2014. A smart contract is a computer program or a transaction protocol which is intended to automatically execute, control or document legally relevant events and actions according to the terms of a contract or an agreement. Smart contracts cannot be deleted or stopped, and transactions cannot be reversed. Ethereum can therefore be regarded as a ‘decentralised computer’.

Smart contracts deliver the DeFi functionality. In the past four years, various base finance functions – such as exchange, lending and borrowing – have been implemented by smart contracts. Computer code has been launched on the Ethereum network, and holders of tokens can participate in transactions directly through a digital wallet (e.g. Metamask, Argent and Trezor). This has led to the emergence of fully automated lending, borrowing and trading markets. The smart contracts merely provide functionality and can operate as ‘Lego blocks’, allowing innovations to be built on top of one another, just like the internet itself is built upon various protocols (TCP, IP, SSL, http, smtp, www, pop, etc). Another similarity with the internet is that there is no entity, so there is no CEO or support desk to contact when things do not work as they should. Despite the fact that it is still early days in this industry and the risks are high, DeFi is achieving tremendous growth.

Regulators are pondering what to do with DeFi. Similar risks apply to DeFi as with traditional finance (TradFi), such as insider trading, cartel-like behaviour and market manipulation. It is not easy to regulate a piece of computer code without a legal entity. Additionally, the permissionless nature of blockchain is a major concern to regulators; people can participate without opening an account for KYC/AML.

|

Cryptocurrencies differ greatly in the way their governance is organised and thus in their level of decentralisation, security and performance. Decentralisation of secure transactions is slow because it requires more coordination between various actors, which is costly and slow. In contrast, centralisation limits the number of actors involved, but requires more trust to be placed in fewer parties.

Bitcoin is at one end of the spectrum (very decentralised: slow, costly but extremely secure), while the company Binance is towards the other end of the spectrum (centralised: fast, cheap and sufficiently secure). Ethereum is somewhere in the middle; experience has shown that it is much easier for a relatively small group of actors to implement changes5 in Ethereum than in Bitcoin, plus more computing resources are needed per node to run Ethereum than Bitcoin, making Ethereum harder to decentralise. |

How DeFi presents opportunities for the financial industry

Over the past decades, the financial ecosystem has evolved into a global maze of payment services, systems and rules involving numerous players, including regulatory and supervisory bodies. How can DeFi be expected to impact on this ecosystem?

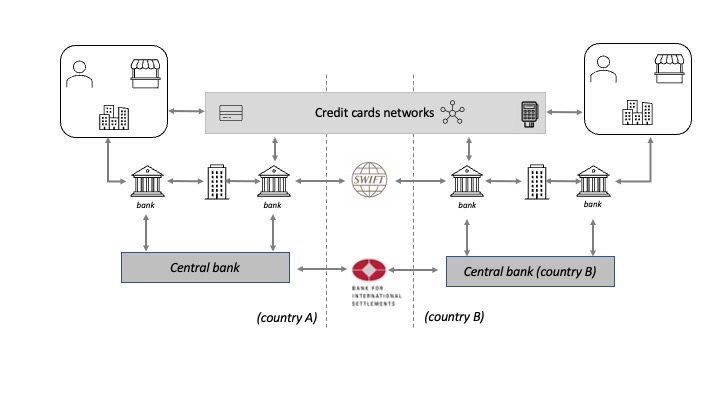

Today’s payments ecosystem can be simplified into the following high-level processes and actors (see Figure 2).

Figure 2 – Simplified representation of the complex and dynamic payments ecosystem.

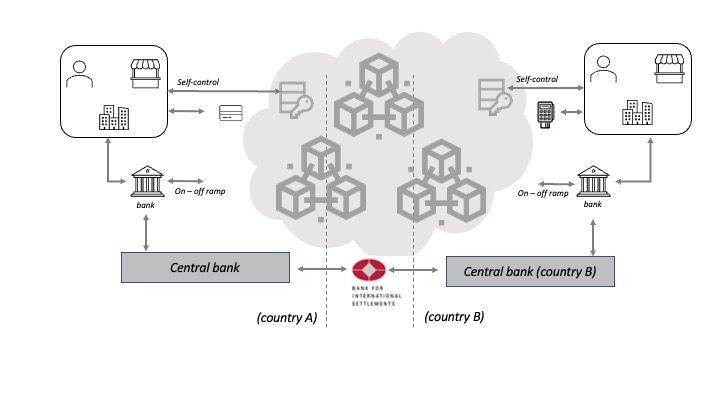

Figure 2 shows the ‘bank-to-bank’ chain of payments for individuals and businesses. The credit card networks are built ‘on top’ of the banking systems so that digital transactions can be performed in any place and at any time, in brick-and-mortar stores and online. DeFi technology has the potential to bypass major parts of this traditional infrastructure. After all, there is a uniform crypto address space all the way down to the individual user, as well as a low threshold for technical and legal participation in the network, which is based on the very latest internet technologies. Figure 3 shows how the payments ecosystem could look in a DeFi world.

Figure 3 – The simplified payments ecosystem in a DeFi world.

This shows that once an asset exists on a blockchain, the user has full ownership and control. Additionally, digital assets can be moved around, irrespective of borders and jurisdictions, and Layer 2 solutions are making this even faster and cheaper.

Moreover, as mentioned above, users can choose to use a service provider to manage keys and access to the various blockchains. However, these service providers have so far tended to be new market entrants. This represents a clear opportunity for the financial sector. A handful of traditional players are now embarking on buying and holding crypto assets (e.g. PayPal in 2020). Moreover, in 2020, the US regulator (Office of the Comptroller) allowed banks to start offering custody services, which opens new avenues for existing players.

More for less

DeFi offers interesting potential to reduce costs and increase speed in payments by eliminating friction in terms of technology, contracting and the coordination between multiple parties. This is expected to impact on many functions of today’s payment and securities market infrastructures, such as clearing houses, RTGS, secure messaging, custody, exchanges and FX services.

Digital assets enable companies to make their idle cash work for them. It is also possible to obtain yield by depositing into decentralised lending pools such as Aave and Compound. The yield is coming from borrowers who take loans against (crypto) collateral. If the value of the collateral drops under a certain threshold, the collateral is automatically liquidated, and the loan is repaid – with no human intervention due to the use of smart contracts.

DeFi holds the promise of faster, better and cheaper payments, yet a number of hurdles need to be overcome, including the regulatory, commercial and technical adoption of this nascent infrastructure.

Nevertheless, this shift offers opportunities for incumbent financial institutions as they already have services and customers in place and seek lower costs and higher quality. An infrastructural change ‘behind the scenes’ does not necessarily have to change the basic user experience, as was demonstrated by voice over IP (VoIP) a couple of decades ago; it just makes the service better by improving quality and reducing the costs. DeFi ‘behind the scenes’ could achieve a similar outcome, with today’s market infrastructure slowly but surely migrating to this more decentralised technology stack.

Examples of DeFi in practice

1. Countrywide payment systems and remittanceIn September 2021, El Salvador government launched a Bitcoin and Lightning-based payment network8 for handling both inbound remittance payments as well as point-of-sale payments. In a matter of months, the service was set up by various independent service providers and banks to provide wallet apps (such as Chivo and Strike) and gateways to the Bitcoin and Lightning network, all based on open-source components.

This initiative has three drivers:

Merchants in El Salvador have updated their cash register software. Users can now choose to hold their wallet balance in US dollars or in Bitcoin and can easily switch between the two, in order to limit exposure to volatility. The liquidity is provided through a government fund.

2. Merchant acceptanceBitpay is one of the first crypto payment acceptance services for merchants. At the moment of a fiat check-out, buyers can choose crypto as their payment method. The Bitpay services calculates the corresponding amount in crypto in real time and displays this to the user. The user pays (e.g. by scanning a QR-code with a wallet app) and confirms the transaction to the merchant. Typically, the merchant receives the amount in fiat from Bitpay.

In November 2021, Regal Group (operator of 500 cinemas across the USA) announced the acceptance of digital tokens for buying movie tickets, popcorn and drinks9. By making use of the Layer 2 Flexa network, Regal allows users to directly spend a wide range of cryptocurrencies, stablecoins and digital tokens (including Bitcoin, Ethereum, Dogecoin, Litecoin, GeminiDollar, DAI, Link, Atom and BAT) from their wallet apps. Users pay by scanning a bar code displayed at the cash register and the transaction is settled instantly. Regal gets paid out in fiat dollar through the regulated part of Flexa.

3. B2B paymentsDeFi offers innovative treasurers ample opportunities. Through a growing number of regulated exchanges, they can use, hold and transfer stable coin values more quickly and cheaply. No negative interest rates apply. More adventurous treasurers are going all in with non-fiat crypto, such as the listed company MicroStrategy led by Michael Saylor. In the summer of 2020, MicroStrategy converted all its excess cash into Bitcoin, which was a major event in the crypto and DeFi community. Since then, more companies have followed suit10, including Tesla and Square. |

verwandte Publikationen

Publication

|

Interview

The European financial sector is entering a new era of data-driven innovation. T...

Lesen Sie mehr

Publication

|

Blog

COMPANIES CAN MAKE PURSUING SUSTAINABILITY MORE SUSTAINABLEMany companies made promises to shareholders and the public to pursue sustainability. While most are trying to fulfill their pledges despite some relaxation in mandates, they aren’t finding it easy. The market has tried to help by developing decarbonization claims that allow busin...

Lesen Sie mehr

Publication

|

Blog

The topic of artificial intelligence dominates boardroom discussions, yet most organizations are struggling to unlock its full potential. Research by RAND shows that up to 84% of AI projects fail to scale to deliver enterprise-wide impact (RAND, 2024). A recent study from MIT reveals even higher figures, finding that 95% of...

Lesen Sie mehr

Publication

|

Blog

In the wake of the digital revolution, the money landscape is rapidly evolving. ...

Lesen Sie mehr

Publication

|

News

A new report commissioned by the Euro Banking Association outlines the strategic...

Lesen Sie mehr

Publication

|

Blog

Stablecoins are entering mainstream finance, offering the potential to make the ...

Lesen Sie mehr